One Size Fits None

Do you have a formal job? If so, you probably have a retirement savings account (RSA) too. Each month, a portion of your salary is sent to this RSA – held with a pension fund administrator (PFA) – and is committed to investments on your behalf. The premise is that by the time you retire, your initial investment and accrued income are sufficient to cater for your post-retirement lifestyle. The process is simple but is a bedrock of modern financial systems and ensures that people do not become reliant on the public purse in old age.

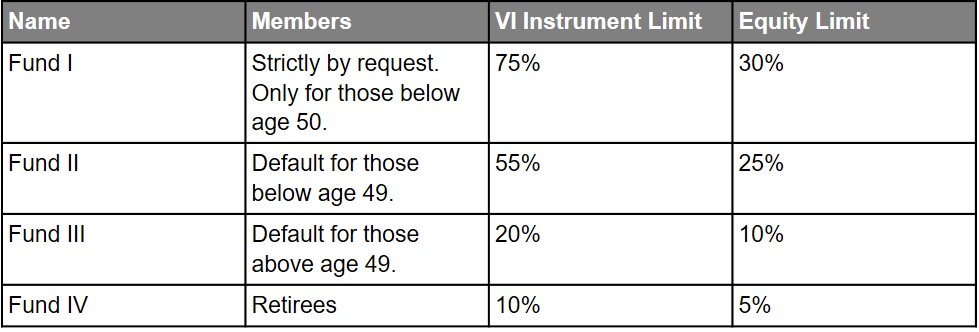

A significant change is now taking place here, one that inadvertently affects you and I. Previously, a single PFA would pool all its RSA accounts – from Tom, Dick, and Harry – into a single fund subject to a set of investment rules. Now, per new PenCom regulations, this single fund structure will be changed to a multi-fund structure. Specifically, PenCom has created four fund classifications governed by different investment rules, the key difference being each fund’s exposure to variable income instruments. Unlike fixed income instruments that pay out a fixed return over time, the returns from variable income instruments fluctuate and are sometimes determined by market forces. A familiar example is an investment in the shares of a public limited company i.e. equity.

The table above shows the impact of the change. At the moment, a maximum of 20% of RSA funds can be invested in equities. Under the new rules, this can now be as high as 75% depending on the fund.

Why should we treat investments differently?

On a basic level, the new regulations make sense. Different employees have RSAs, and each has her own risk appetite, depending on age, lifestyle, wealth, and other factors. Treating all these people as if they were one investor makes little sense. With the new rules, a 60-year old man looking to retire soon can rest in the assurance that his RSA will be invested in the safest assets to guarantee his capital is returned to him at the very least. Meanwhile, a 25-year old woman in her first professional job will be happier knowing that her pension contributions are seeking high risk-adjusted returns, considering she is unlikely to tap into them for many decades.

The old rules were inefficient because they did not allow fund managers differentiate between people. The multi-fund structure makes it more likely that they will be able to develop investment strategies to satisfy the needs of a wider range of RSA holders. It also gives PFAs greater flexibility. For example, a pot of ₦50 million under Fund I can be dedicated to a mix of equity investments (30%), REITs (15%), corporate debt (15%), private equity funds (10%), infrastructure bonds (10%), government securities (20%) while an identical pot under Fund IV would look more like a mix of corporate debt (20%), equity instruments (5%), REITs (5%), and gogvernment securities (70%). The latter is more conservative while the former should earn higher returns in the longterm.

There is another key benefit of the new regulations, albeit an indirect one. Allowing PFAs greater exposure to variable income instruments will help deepen Nigeria’s financial markets. Presently, fixed income dominates the markets. We can expect to see PFAs diversifying more into the equity market, as well as alternative investments like REITs and infrastructure funds.

Why is this good?

Investors and savers (us) benefit from a wider range of investment vehicles and capital raisers (e.g. companies) also benefit from a wider range of capital-raising opportunities. Diversity helps spread risk while greater participation improves liquidity, all of which would further develop Nigeria’s financial markets and fuel economic growth and financial awareness.

In spite of the benefits, PFAs can feel justifably aggrirved by these changes as fixed income investments have been extremely profitable for many years. At its April Auction, the Federal Government sold its new 20-year bond at an interest rate of 16.25% per year. Meanwhile, if you had invested in the entire basket of stocks on the Nigerian Stock Exchange at the start of the year, chances are you would be down on your money – the market has lost 2.63% year-to-date. Add in the fact that Nigeria’s historically high inflation means that interest rates and fixed income yields tend to be high and you can understand why many PFAs prefer to stick to fixed income investments.

Will variable income investments bring comparable returns?

On paper, they should. To compensate for their variable nature, they ought to have a higher payoff. This has not often been the case in Nigeria, and many investors are still smarting from when the stock market crashed in 2008/2009. Investor education will be crucial to ensure that market participants understand the instruments they are exposed to (who knows how a REIT works?) and are able to analyse their economic viability.

This may be the long run impact of the new regulations – increasing interest in alternative investments and deepening the capital markets. When this happens, investors – and people like you and I – will truly be able to benefit from a more diverse portfolio, whether through their RSAs or personal portfolios. The multi-fund structure is an important step in that direction yet isn’t quite complete. I would hope that in a few years, there will be even greater flexibility in how RSAs can be invested.

Subscribe to read more articles here.