Two charts looking at peer-to-peer lending in Nigeria

This article was produced on behalf of FINT, one of Nigeria's leading peer-to-peer lending companies, as we explore marketplace lending in Nigeria.

The promise of high returns on your investment is undoubtedly the most attractive part of FINT and other peer-to-peer (P2P) lenders. This is true both in Nigeria and abroad. While The Lending Club and Prosper, some of the world’s largest P2P lenders, give returns of nearly 8% and 12%, FINT offers you returns almost as high as 40%; significantly higher than what you would earn abroad.

Unsurprisingly, FINT outperformed basically all local formal investment channels in 2017.

Even though the Nigerian stock market enjoyed a bumper year where it gained 42% (the 5th highest market return since 2000), an investment on the FINT platform would still have fared a bit better than investing in the MSCI Index—the largest global tracker of the Nigerian stock market. In addition, FINT easily outperformed the safest long-term investment (government bonds).

Can we expect the same thing in 2018? Perhaps. The Nigerian stock market was already down more than 7% near the end of August, and interest rates are barely touching 15% even after a recent rise.

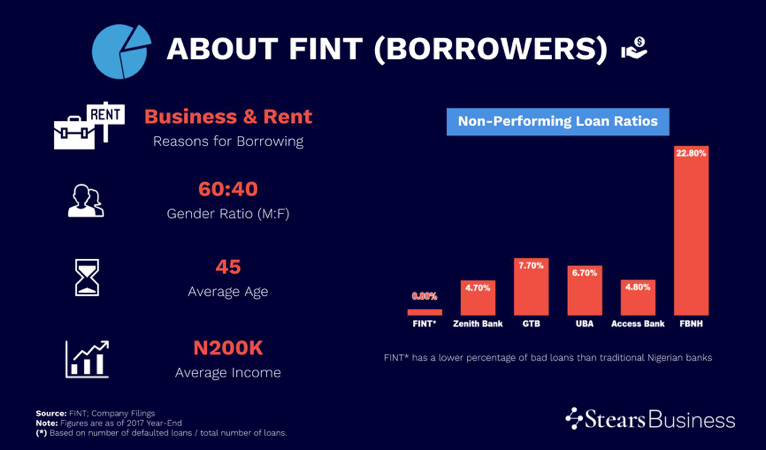

A snapshot of borrowed related data on FINT's platform.

Non-performing loans—those the borrower has not paid interest on recently or doesn’t look like they will be able to repay—have been topical in Nigeria for a long time. We even spoke about them in early 2017.

It’s interesting to see that FINT’s default rate (or NPL ratio) is much lower than Nigeria’s top banks (0.8%). Even accounting for the fact that intense CBN regulation means that banks are likely to be much more prudent in recording bad loans, the margin between FINT and other big banks like First Bank (22.8%), Diamond Bank (12.3%), and FCMB (5.7%) is quite wide.

One way this can improve is if FINT refines its credit rating system enough so that it can screen bad borrowers. This will improve the quality of the borrowing pool and reduce the likelihood of loans going bad. Of course, if Nigeria’s big banks figure out how to screen prospective lenders (corporates and individuals) better, then they stand to benefit even more.

Finally, look closely at the infographics, and you’ll notice that the demography of lenders and borrowers is pretty similar. The average age is around the same, and much higher than you may have expected for a technology-based platform, perhaps underscoring how intuitive and straightforward the P2P model is.

You would not be surprised to see the gender ratio skewed towards men; but is it because they tend to be more risk-seeking or because they are more likely to be covering business expenses and school fees, the two most cited reasons on the FINT platform?

The average investment or loan is actually still quite small (₦200,000) and evidence abroad shows that P2P lending can process much larger numbers over time; the Lending Club has facilitated loans of over $35 billion since inception - almost 10% of the Nigerian economy. The crucial thing for FINT is ensuring that their trusted screening methods and platform framework work as smoothly with transactions of ₦20 million as they do for ₦200,000.

To learn more about FINT's services, head over to their marketplace or read more Stears content on FINT.